Chris Bailey, European Strategist, Raymond James Euro Equities*

“Emerging markets are hugely important” James Dyson

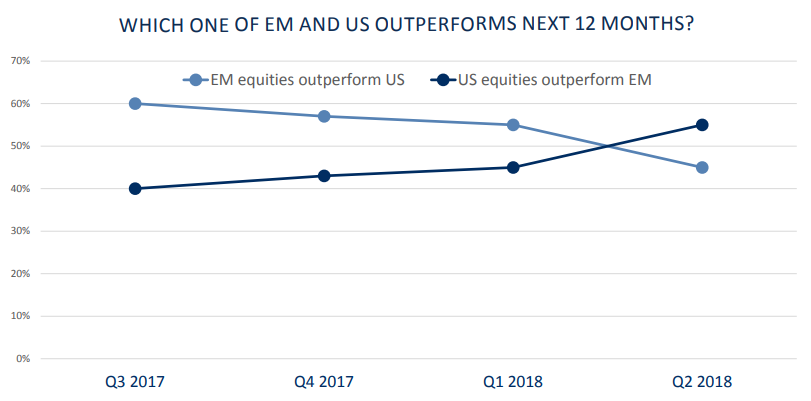

In the world of emerging market investments it tends to either be feast or famine. Whilst the second half of 2016 and especially 2017 proved to be the latter, the first half of 2018 has proved to be somewhat more challenging. And it has not mattered one iota if you are an equity, fixed income or local currency investor – all have struggled at an aggregate emerging markets index level.

As with anything in the world of investments, there is the general and there is the specific. The biggest general (negative) influence on emerging markets during 2018 has been the appreciation of the US dollar. There are many reasons why emerging markets do not like a rising dollar, from higher interest rate burdens on dollar-denominated debt, to (typically) lower commodity sale prices plus the general tightening of global liquidity a higher dollar tends to stand for. During 2018 the higher dollar has also reflected a defensive shift by some international investors worried about rising trade tensions. Key emerging markets such as China and Mexico have been in the direct firing line of the ‘fair trade’ rhetoric and wishes of the US administration, a reality which has intensified concerns. Beyond investors booking some profits and dollar/trade issues, specific issues across a number of intermediate sized emerging markets have had an influence. Argentina requested formal assistance from the International Monetary Fund (IMF), whilst Turkey’s combination of deficits and inflation led to high volatility. Both Russia and Iran have been impacted by economic sanction decisions led by the US administration whilst Brazil, Hungary and the Philippines have seen their local stock markets move into bear territory (a fall of 20%+).

The local Chinese stock market has also been flirting with bear market territory as the last thing the world’s biggest emerging market needs is a slowdown in the rate of its economic growth. As noted above, trade concerns have started to impact the country and this has the capability to put pressure on China’s ability to keep changing at a breakneck speed and hence, in turn, being the world’s largest consumer at-themargin of many commodities.

However it is not all about demand… sometimes it can be about change too. Despite trade concerns, lowered expectations and specific country level disappointments, the biggest positive for emerging markets today remains the journey from a ‘frontier’, to ‘emerging’ and finally a ‘developed’ economy. Themes centred on urbanisation, the growth of a middle class, heightened consumerism, more effective and less corrupt government, among many others still provides a heady strategic attraction which any international investor with a mediumterm outook still really needs to be exposed to. Additionally, current valuation levels for both emerging market equity and debt markets look attractive against more developed market equivalents. Meanwhile, sentiment surveys show waning investor attraction towards emerging markets boosting the attraction for more contrarian minded investors.

By definition it can be hard to generalise about an area as diversified as emerging market investment. However, thinking at an index level, tactically, trade rhetoric and realities and the level of the US dollar will prove highly influential over the balance of this year for the area. With many emerging markets – especially the influential China – showing a stronger commitment to economic reform and change than their developed market cousins, investor caution should only really extend so far. Today I would rate broader emerging market indices as offering more opportunity than threat.

You can read more articles from Chris Bailey and the Raymond James Investment Strategy Committee in the July edition of Investment Strategy Quarterly

*An affiliate of Raymond James & Associates and Raymond James Financial Services

DISCLAIMER: The information contained in this article is for general consideration only and any opinion or forecast reflects the judgment of the Research Department of Raymond James & Associates, Inc. as at the date of issue and is subject to change without notice. Past performance is not a reliable indicator of future results.

You should not take, or refrain from taking, action based on its content and no part of this article should be relied upon or construed as any form of advice or personal recommendation. The research and analysis in this article have been procured, and may have been acted upon, by Raymond James and connected companies for their own purposes, and the results are being made available to you on this understanding.

Neither Raymond James nor any connected company accepts responsibility for any direct or indirect or consequential loss suffered by you or any other person as a result of your acting, or deciding not to act, in reliance upon such research and analysis. If you are unsure or need clarity upon any of the information covered in this article, please contact your wealth manager.

Black MondayOn 19 October 1987, the stock markets experienced a dramatic plunge that prompted many firms to shut down their trading desks and turn off their phones to minimize internal losses. Raymond James refused to do the same. Our desks stayed open to help meet clients’ needs, resulting in our first and only unprofitable quarter since the firm went public in 1983. |

|

Who was Raymond James?The Raymond in our name is actually from Edward Raymond, owner of a 15-employee mutual fund sales group, Raymond and Associates, along Florida’s west coast. He sold his company to Bob James on 15 July 1964, on condition that the surviving firm be called Raymond, James & Associates. Three days after the sale, Ed Raymond was involved in a near-fatal automobile accident and never joined the firm. Nonetheless, even after Raymond had passed away, Bob James insisted that his name remain on the door – ahead of James’ own. That was a promise he made to Ed Raymond three days before the accident, and Bob James was a man who kept his promises. |

|

Bear market of 1974The severe bear market of 1974 threatened the existence of Raymond James, which was bleeding capital by the day. Tom James, his father and other leaders took extreme measures to keep the firm afloat, slashing costs, forgoing pay checks and even attempting to sell the firm for just enough capital to protect client assets and retain as many associates as possible. The story could have ended very differently if not for a sharp upturn and continued rebound in the stock markets late in the year. |

|

Taking Raymond James PublicWhen consideration was being given to taking Raymond James public, Tom James penned a letter to shareholders (largely employees at the time). ” … the public offering should be considered as a statement of our independence. While this is a psychological rather than an economic rationale, it is nonetheless very important. We have asserted for some time that we are not interested in becoming a small part of a very large corporation. That assertion results mainly from the inclinations of management rather than the economic benefits associated with either alternative. The public stock offering affords us the opportunity to enjoy a little bit of the best of both worlds. While shareholders will be given liquidity at fair market value, we will still have the ability to control our own destiny.” After 40+ years of Tom’s leadership, upon becoming CEO, Paul Reilly was often questioned about whether the company might ultimately surrender its cherished independence and be acquired by some larger entity. His response: “Not while I’m around.” It’s a theme that continues today. |

|